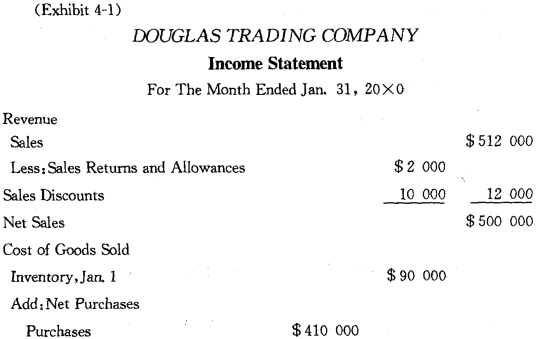

Income Statement is designed to portray the operating results for a period of time. Exhibit 4-1 is the income statement of Douglas Trading Company for the month ended January 31,20X0.

The major categories of the income statement for a merchandising company are revenue, cost of goods sold and operating expenses. In the revenue section, sales returns and allowances and sales discounts are deducted from the gross sales to yield net sales. The cost of goods sold is obtained by adding the beginning inventory and net purchases and deducting the ending inventory. To calculate net purchases, we deduct purchases returns, allowances and discounts from the purchases amount and add transportation costs of purchased goods. By deducting the cost of goods sold from the net sales,we arrive at an intermediate amount called gross profit on sales. The operating expenses are then deducted from the gross profit on sales to obtain the net income for the period.

The operating expenses of a merchandising business are typically classified into selling and administrative expenses. Some business items affecting the determination of a final net income amount may not relate to the primary operating activity of the business. Interest income and interest expense, for example, may be viewed as relating more to financing and investing activities than to merchandising efforts. They are often shown in a separate category called “Financial Income and Expense” at the bottom of the income statement. Likewise,any extraordinary items, such as catastrophic loss from an earthquake, will be shown in a separate “Extraordinary Items”category before the final net income amount is figured. Douglas Trading Company had no transactions or events to list in either of these categories on its income statement.

Operating results summarized by the income statement will be reflected in the owners’ equity section on the balance sheet at the end of that period. For yearly financial statements, the complementary relationship might be shown graphically as follows:

Dec. 31,20X0 Year 20X1 Dec. 31, 20X1 Year 20X2 Dec. 31,20X2![]()

The financial statements illustrated in this text are all prepared on the accrual basis.

New Words, Phrases and Special Terms

Notes to the Text

1.Interest income and interest expense, for example, may be viewed as relating more to financing and investing activities than to merchandising efforts.

(1)for example 是插入语。

(2)作为介语as的宾语的动名词短语relating more to…than to…,用more…than连接起来,形成对比结构。relate后要接用介词to.

2. Likewise, any extraordinary items, such as catastrophic loss from an earthquake,will be shown in a separate "Extraordinary Items”category before the final net income amount is figured.

(1)全句包含一个用连词before引导的时间状语从句。

(2)such as catastrophic loss from an earthquake 是句中主语any extraordinary items 的同位语。

3. Operating results summarized by the income statement will be reflected in the owners’ equity on the balance sheet at the end of that period.

过去分词短语summarized by the income statement修饰句中主语operating results。

READING MATERIAL

WORKING CAPITAL AND SHORT - TERM LIQUIDITY ANALYSIS

A company’s short-term liquidity (短期偿债能力) refers to its ability to meet short-term obligations. The working capital (菅运资本),which is the difference between a firm’s current assets and current liabilities,is a significant figure, because it represents the net current capital with which the firm conducts its operations. Insufficient working capital may prevent a firm from meeting its debts on time. Sometimes, when a company borrows using long-term notes or bonds, the lender requires the borrower to maintain a stipulated amount of working capital.

In analyzing a company’s short-term liquidity,we can calculate various working capital ratios. These ratios include:

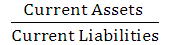

Current Ratio(流动比率)=

This ratio is a measure of the firm’s ability to meet its current obligations on time and to have funds readily available for current operations. For many years,some short-term creditors have relied on a rule of thumb (拇指,法则,经验规律)that the current ratio for industrial companies should exceed 200%.

Sometimes analysts calculate the ratio between the liquid or“quick”,current assets and the current liabilities. The quick ratio may give a better picture than the current ratio of a company‘s ability to meet current debts. When taken together with the current ratio,it gives the analyst an idea of the influence of the inventory figure in the company’s working capital position.

Quick Ratio(速动比率)=

The inventory turnover ratio measures the average rate of speed inventories move through and out of company. Inventory turnover is computed as:

Inventory Turnover(存货周转率)=

Of course,a low inventory turnover can result from an overextended inventory position or from inadequate sales volume. For this reason,appraisal of inventory should be accompanied by scrutiny of the quick ratio and analysis of trends in both inventory and sales to find out what has occurred. Inventory turnover figures vary considerably from industry to industry, and analysts frequently compare a firm’s experience with industry averages.

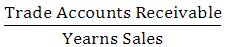

The average collection period is used to determine the number of days it takes,on average to collect accounts (and notes) receivables. It is calculated as:

Average Collection Period(平均收账期)=

A rough rule of thumb sometimes used by credit agencies is that the average collection period should not exceed 1. 5 times the net credit period. With the figure in Douglas Company’s balance sheet on January 31,20X0 and the income statement for the month of January, 20X0 we get:

(1)Working capital= $ 202 000 — $ 79 000= $ 123 000

(2)Current ratio= = 2. 56 or 256%

= 2. 56 or 256%

(3)Quick ratio = =1.25 or 125%

=1.25 or 125%

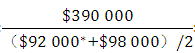

(4) Inventory turnover= =4.11 times

=4.11 times

* the supposed amount of beginning inventory.

(5) Average collection period= X 365=24. 82 days

X 365=24. 82 days

| 以上信息有错误 |