Many companies employ a method of controlling expenditures that is known as the voucher system. Under this system, a written authorization form, called a voucher, is initiated for every disbursement the firm makes. Before the designated responsible official approves the voucher for payment, several verification steps must be performed by different employees. These include the following (for the purchase of merchandise):

(1) Comparison of purchase order, invoice and receiving report for agreement of quantities, prices, type of goods, and credit terms.

(2) Verification of extensions and footings on invoice.

(3) Approval of account distribution (items to be debited).

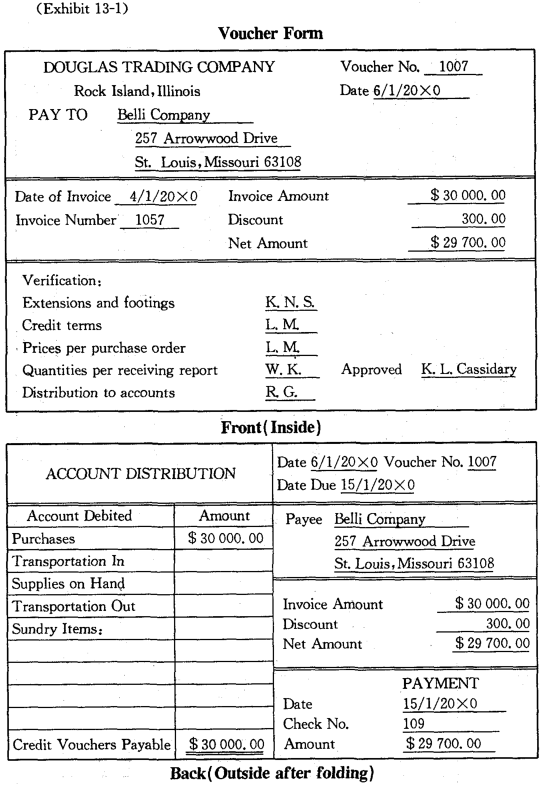

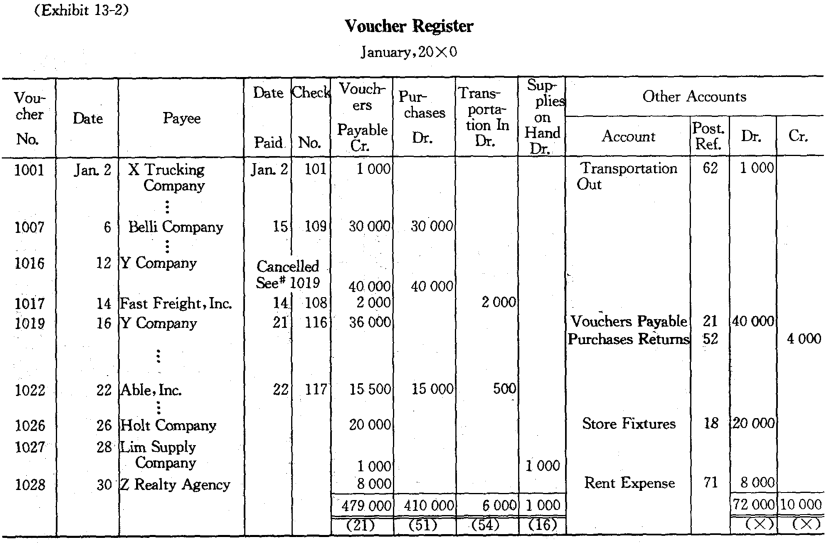

A voucher form is illustrated in Exhibit 13-1. The original copies of the purchase order, invoice and receiving report should be attached to the voucher. The voucher is then recorded in a book of original entry called the voucher register, which replaces the purchases journal (invoice register) we illustrate in Lesson Seven. A simple form of voucher register is provided in Exhibit 13-2. The entries recorded are from the same transactions given in Lesson Seven (with voucher # 1007 added in).

Note that:

(1) Since all expenditures are recorded in the voucher register whether the transaction is for cash or on account, the voucher register also substitutes for part of the cash disbursements journal illustrated in Lesson Seven.

(2) The most formal method of processing purchases returns and allowances under a voucher system is to cancel the original voucher and issue a new one for the lower amount (see vouchers # 1016 and # 1019).

Vouchers are entered in the voucher register in sequence. Then they are filed in an unpaid vouchers file in the order of required date of payment. In this way, cash discounts will not be missed and the company's credit standing will not be impaired.

On the due date, the voucher is removed from the unpaid file and forwarded to the firm's disbursing officer for final approval of payment. After signing the voucher, this officer has a check drawn and mailed to the payee. To safeguard against irregularities, the voucher should not be handled again by those who prepared it, and the underlying documents should be cancelled or perforated under the control of the disbursing officer before the voucher is returned to the accounting department.

After a voucher is paid,the check number and payment date are entered in the appropriate columns of the voucher register. Therefore,it is easy to determine the total unpaid(“open”)vouchers at any time by adding the items in the vouchers payable column for which there is no entry in the date paid and check number columns (see vouchers # 1026, # 1027, # 1028). This total should, of course, agree with the total of vouchers in the unpaid file and, at the end of the month, with the amount in the Vouchers Payable account.

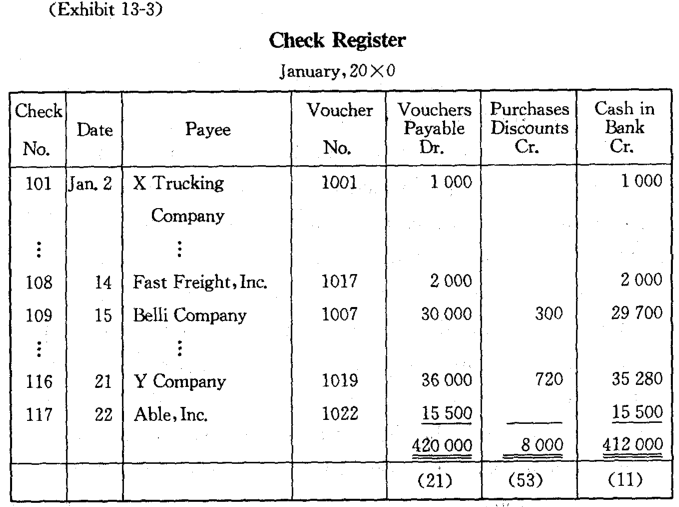

After these procedures have been followed, the payment is recorded in a book of original entry called the check register, which is used in place of a cash disbursements journal. Finally, the vouchers are filed in numerical sequence in a “paid” vouchers file.

New Words, Phrases and Special Terms

- authorization(n.) 授权

- voucher system 应付凭单制

- approve (v. t.) 批准

- verification(n.) 验证

- extension(n.) 算出或转来的金额

- footing(n.) 总计,总额

- purchase order 定货单,定购单

- receiving report 收货报告,收货单

- voucher register 应付凭单登记簿

- replace(v.t.) 取代

- sundry items 其他项目

- in sequence 按顺序,依次

- credit standing 信用地位,信誉

- perforate(v.t.) 穿孔于

- in place of 代替

Notes to the Text

1. The voucher is then recorded in a book of original entry called the voucher register, which replaces the purchases journal we illustrate in Lesson Seven.

(1)非限制性定语从句which replaces…修饰voucher register。

(2)在这一定语从句中,还包含一个修饰purchases journal 的定语从句(that)we illustrate…,关系代词that因在从句中作谓语动词illustrate的宾语,可省略。

2. Since all expenditures are recorded in the voucher register whether the transaction is for cash or on account,the voucher register also substitutes for part of the cash disbursements journal illustrated in Lesson Seven.

(1)全句包含一个用连词since引导的原因状语从句。

(2)在这一状语从句中,还包含一个用连词whether引导的条件状语从句。

(3)过去分词短语illustrated in…修饰the cash disbursements journal。

3. To safeguard against irregularities,the voucher should not be handled again by those who prepared it, and the underlying documents should be cancelled or perforated under the control of the disbursing officer before the voucher is returned to the accounting department.

(1) 用连词and连接的并列句。不定式短语to safeguard against irregularities表示目的,修饰全句。

(2) 在前一个并列分句中,包含一个修饰those的定语从句who prepared it。

(3) 在后一个并列分句中,包含一个由连词before引导的时间状语从句。

4. Therefore, it is easy to determine the total unpaid (“open”) vouchers at any time by adding the items in the Vouchers Payable column for which there is no entry in the date paid and check number columns.

(1) 全句中,it是形式主语,真正主语是不定式复杂结构to determine…。

(2) 在这一不定式复杂结构中,包含一个用介词引导的复杂结构by adding…,其中介词by的宾语是动名词复杂结构adding the items in…。

(3) 在这一动名词复杂结构中,包含一个修饰the items的定语从句。关系代词which在从句中作介词for的宾语。

READING MATERIAL

INTERNAL CONTROL IN OTHER AREAS

While it is vitally important to establish effective controls over the handling of and accounting for cash, control should also be provided for other activities of the firm. As in the case of cash, most controls are designed to separate the authorization of a transaction from the accounting for the transaction and the custody of any related assets. For example, the purchase and sale of securities normally require authorization by a company’s board of directors, and officers who have access (接近)to the securities should not have access to the accounting records. Other personnel should record security transactions and keep a record of security certificates by certificate number and amount.

Similarly, in the case of inventories, store(仓库) clerks handling inventory items should not have access to inventory records and should be separated from receiving departments and the processing of accounts payable. Similar controls should be exercised over receivables, long-term assets,payroll(工薪)transactions, and every other fact of business activity.

The subject of internal control is quite complex. Both external and internal auditors(审计员) devote a great deal of attention to internal control In analyzing an accounting system and preparing audits.

| 以上信息有错误 |