Promissory notes are often used inmerchandise and property transactions, particularly when the credit period is longer than the typical 30 or 60 days for open accounts. Occasionally, a note is substituted for an open account when an extension of the usual credit period is granted. In addition, promissory notes are normally executed when loans are obtained from banks and other parties.

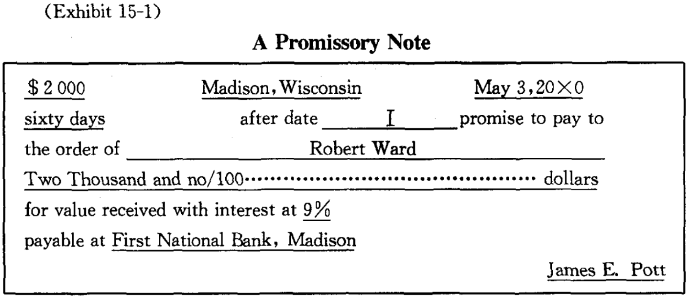

A promissory note is a written promise to pay a certain sum of money on demand or at a fixed and determinable future time. The note is signed by the maker, and it is made payable either to the order of a specific payee or to the bearer. The note may be noninterest bearingor it may be interest bearing at an annual rate specified on the note. An interest-bearing promissory note is illustrated in Exhibit 15-1.

(A note held from a debtor is called a note receivable by the holder and a note payable by the debtor. A note is usually regarded as a stronger claim against a debtor than an open account because the terms of payment are specified in writing. Although open accounts can be sold (factored), it is much easier to convert a note to cash by discounting it at a bank.

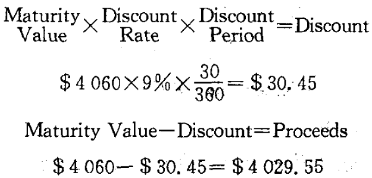

Interest on notes is commonly paid at the maturity date of the obligation, except in certain discounting transactions. Occasionally,a business may prefer not to wait until the maturity date of a note receivable to obtain cash from the customer. Instead, it will endorse the note over to a bank, ‘‘discounting” the note and receiving an amount equal to the maturity value of the note less the discount charged by the bank. By endorsing the note (unless it is endorsed ”without recourse”), the business agrees to pay the note at the maturity date if the maker fails to pay it . Consequently, the note is a contingent liability of the endorser. The discount computation and calculation of proceeds for a $ 4 000, 60-day, 9% note dated March 1 and discounted at 9% on March 31 is as follows:

The discounting transaction should be recorded as follows:

March 31 Cash 4 029.55

Interest Income 29. 55

Notes Receivable Discounted 4 000. 00

The Notes Receivable Discounted account credited in the above entry is a contra account that is subtracted from the Notes Receivable account in the balance sheet. Only the notes still held by the company are added to the current assets total. Some firms do not exhibit the Notes Receivable Discounted account in the balance sheet; instead, they show the notes still held, with a footnote to this item under the balance sheet indicating the contingent liability.

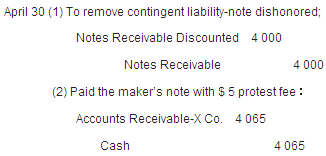

When the maker of a discounted note receivable pays the note at maturity, the discounting party (endorser) may then remove the note receivable amount and the contingent liability contra amount in Notes Receivable Discounted from its accounts. If the maker of a note receivable fails to pay it (dishonors it)at maturity, the bank will notify the endorsing party and charge the full amount owed, including interest, to the bank account of the endorser. In addition, the bank may also charge a small fee called a protest fee. Two entries would be made by the endorser:

If the endorser failed in its efforts to collect the $ 4 065 from X Company, the account would be written off as uncollectible.

When a business borrows from a bank by giving its own note, the bank often deducts the interest in advance. With this type of transaction, a business is said to be “discounting its own note”. The entry to record this transaction would be:

Dec. 16 To discount our 60 day note at 9%:

Cash 7880

Discount on Notes Payable 120

Notes Payable 8 000

Discount on Notes Payable is a contra account whose balance is subtractedfrom the Notes Payable amount on the balance sheet. As the time period for the note elapses, the discount is reduced and charged to Interest Expense. Thus, on December 31,after 15 days have elapsed, $ 30 would be charged to Interest Expense and credit to Discount on Notes Payable before the balance sheet is prepared.At the close of an accounting period, it is also necessary to make adjusting entries to reflect the accrued interest income on notes receivable held and accrued interest expense on notes payableoutstanding.

New Words, Phrases and Special Terms

Notes to the Text

1. Promissory notes are often used in merchandise and property transactions,particularly when the credit period is longer than the typical 30 or 60 days for open accounts.

(1)全句包含一个用连词when引导的时间状语从句。

(2)这一时间状语从句中,又包含一个用比较级形容词longer和由连词than引导的状语从句来表示对比。从句中的谓语可省略。即the credit period is longer than the typical 30 or 60 days for open accounts(is long),事实上,只需要掌握住对比两方在句中的对等地位,就能理解这种句型。

2. A note is usually regarded as a stronger claim against a debtor than an open account because the terms of payment are specified in writing.

(1)主句也属于比较结构,对比的是:A note和 an open account 哪一个是较强的要求权。由连词than引导的比较状语从句中的谓语(is regarded as a strong claim against a debtor)被省略了。

(2)全句还包含一个由连词because引导的原因状语从句。

READING MATERIAL

NOTES AND INTEREST IN FINANCIAL STATEMENTS

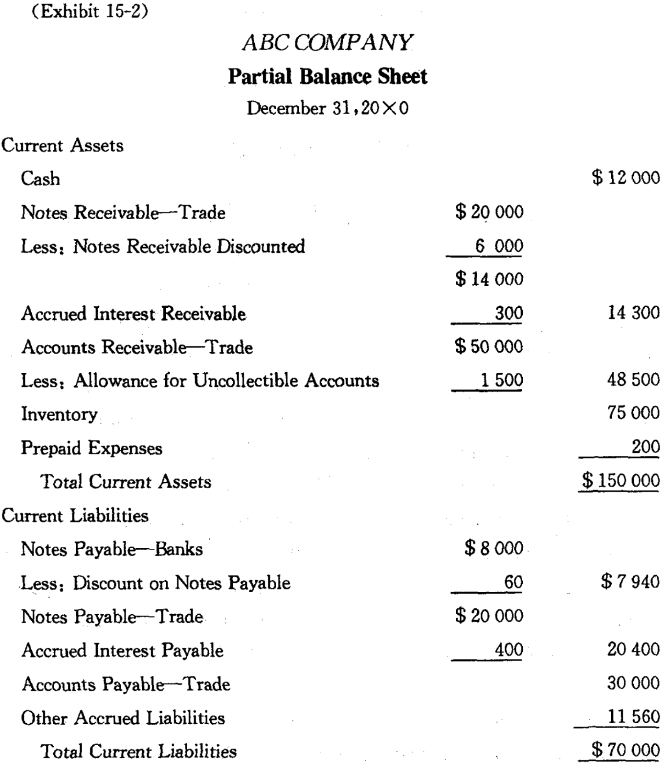

A business will show short-term trade notes receivable as current assets in the balance sheet, because they can normally be converted to cash fairly easily. These notes usually are placed above trade accounts receivable. As with accounts receivable, it is best to separate notes from officers and employees and notes representing advances to affiliated companies from trade notes receivable. If such notes are not truly short-term in character, they should be classified under a heading other than current assets. Accrued interest receivable is normally shown with notes receivable.

Sometimes companies with a large volume of notes receivable find it necessary to provide for possible losses on notes. Frequently, the provision for credit losses is extended to cover losses on notes as well as on open accounts. In such cases, the Allowance for Uncollectible Accounts is deducted from the sum of Accounts Receivable and Notes Receivable in the balance sheet.

Trade notes payable and notes payable to banks are usually shown separately in the current liabilities section of the balance sheet. Accrued interest payable is normally shown with Notes Payable-often as an addition. Discount on Notes Payable is deducted from the related Notes Payable amount. The order in which current payables appear is less important than the sequence of current assets:however, Notes Payable customarily precedes Accounts Payable.

A current section of a balance sheet is shown below to illustrate the presentation of items discussed.

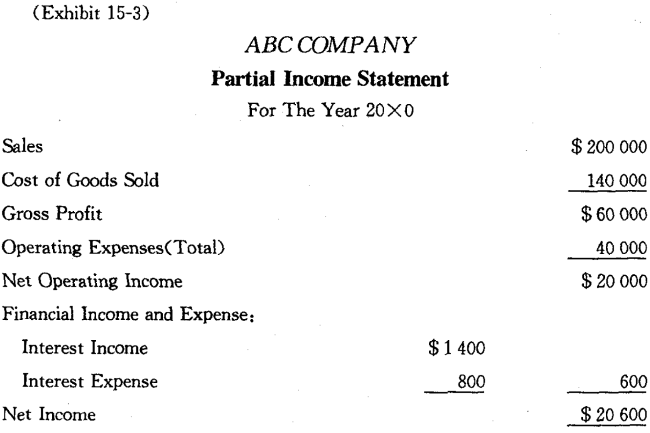

Because they are financial rather than operating items,we often separate Interest Expense and Interest Income from operating items in the income statement.As we see in the Exhibit 15-3, they frequently appear under the classification Financial Income and Expense. This type of presentation permits readers to make intercompany comparisons of operating results that are not influenced by financing patterns(理财方式) of the companies involved.

| 以上信息有错误 |