When preparing financial statements for external users, firms may elect either to prepare a statement of changes in financial position on working capital basis or to prepare a statement of cash flows.

The management of cash flows is a critical function in the operation of a business enterprise. The statement of cash flows may be prepared and used internally as part of the process of planning and controlling cash movements. Cash budgets are also important to the management of cash flows. Our focus here, however, is on cash flow statements prepared for users external to the business.

In 1987,The Financial Accounting Standards Board of U. S. A. issued SFAS No. 95"Statement of Cash Flows”, which superseded APB Opinion No. 19"Reporting Changes in Financial Position". It requires a statement of cash flows as part of a full set of financial statements for all business enterprises in place of a statement of changes in financial position (working capital basis).

This statement requires that a statement of cash flows classify cash receipts and payments as according to whether they stem from operating, investing, or financing activities.

SFAS No. 95 encourages enterprises to report cash flows from operating activities directly by showing major classes of operating cash receipts and payments (the direct method). Enterprises that choose not to show operating cash receipts and payments are required to report the same amount of net cash flows from operating activities indirectly by adjusting net income to reconcile it to net cash flows from operating activities (the indirect or reconciliation method) by removing the effects of (1) all deferrals of past operating cash receipts and payments and all accruals of expected future operating cash receipts and payments and (2) all items that are included in net income but do not affect operating cash receipts and payments. If the direct method is used, a reconciliation of net income and net cash flows from operating activities is required to be provided in a separate schedule.

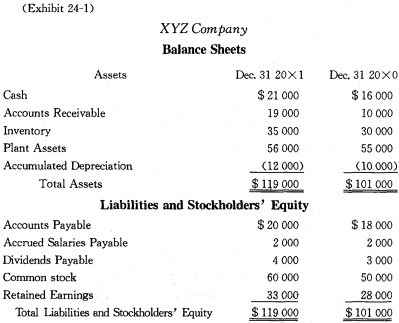

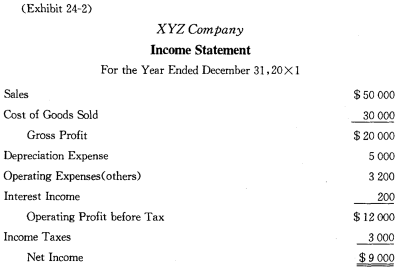

The comparative balance sheets and income statement for the XYZ Company are presented in the following exhibits respectively.

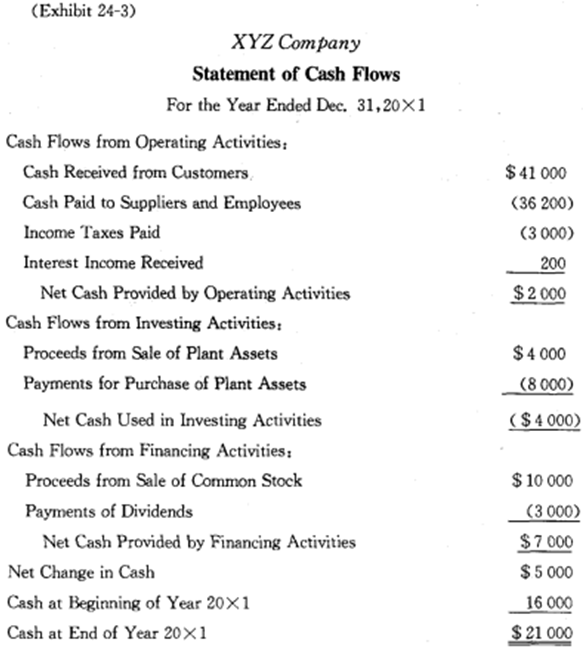

The Statement of Cash Flows of XYZ Company for the year 2000 is presented below:

Reconciliation of Net Income to Net Cash Provided by Operating Activities :

To determine cash received from customers and cash paid to suppliers and employees, one must convert individual revenues and expenses from an accrual to a cash basis. These procedures may be portrayed as follows:

1. Cash Received from Customers=Net Sales+(Beginning-Ending Notes and Accounts Receivable)

In our example:

$ 41 000= $ 50 000+( $ 10 000-$ 19 000)

2. Cash Paid to Suppliers and Employees=[Cost of Goods Sold + (Ending- Beginning Inventories) +(Beginning - Ending Notes and Accounts Payable)] +[Operating Expenses except depreciation and similar write-offs +(Ending- Beginning Deferrals) +(Beginning-Ending Accruals)]

In our example:

$ 36 200=[$ 30 000+( $ 35 000 — $ 30 000) +( $ 18 000 -$ 20 000)] +[ $ 3 200+( $ 0-$ 0) +( $ 2 000 -$2 000)]

New Words, Phrases and Special Terms

Notes to the Text

1. This statement requires that a statement of cash flows classify cash receipts and payments as according to whether they stem from operating, investing, or financing activities.

(1)连词that引导的从句是主句谓语动词require的宾语。从句中的谓语动词classify属祈使语气,其前的should可省略。

(2)上述宾语从句中,还包含一个用连词whether引导的从句,作为 according to 的宾语。

2. Enterprises that choose not to show operating cash receipts and payments are required to report the same amount of net cash flows from operating activities indirectly by adjusting net income to reconcile it to net cash flows from operating activities (the indirect or reconciliation method) by removing the effect of (1) all deferrals of past operating cash receipts and payments and all accruals of expected future operating cash receipts and payments and (2) all items that are included in net income but do not affect operating cash receipts and payments.

(1)关系代词that引导的定语从句that choose…payments修饰全句主语Enterprises.

(2)全句谓语动词are required系被动语态。这种被动结构的句型,实际上是把主动结构句型中复合宾语内的宾语enterprises变为主语,补语不定式复杂结构to report…则保持不动。

(3)这一不定式复杂结构中,以介词by引导的状语修饰整个不定式复杂结构。by的宾语是一个动名词复杂结构,动名词adjusting的复合宾语,由宾语net income和补语to reconcile…这一不定式复杂结构组成。

(4)在上述动名词复杂结构中,又包含一个以介词by引导的状语,修饰整个动名词复杂结构。by的宾语又是一个动名词复杂结构removing the effect…。其后由介词of引导的定语修饰effect,它也是一个复杂结构。

(5)of 的并列宾语all deferrals…and all accruals…与all items…用连词and连接。修饰all items的是关系代词that引导的定语从句,这一定语从句中的并列谓语are included…与do not affect…则用连词but连接。

READING MATERIAL

ANALYSIS OF OPERATING PERFORMANCE

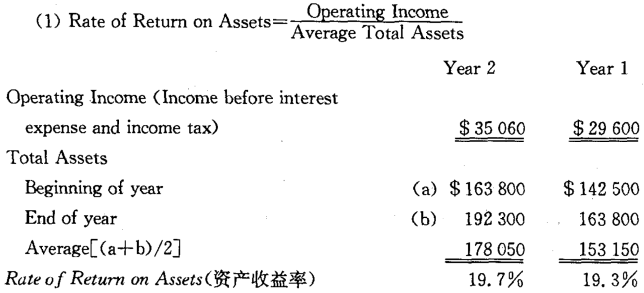

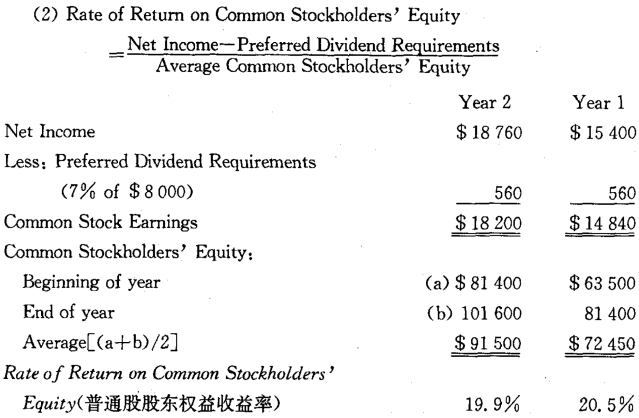

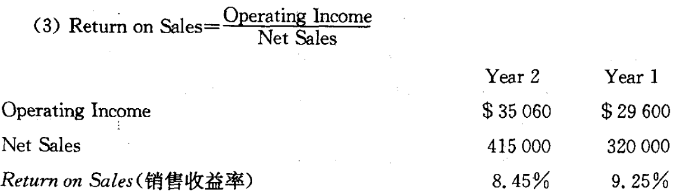

In evaluating the operating performance (经营业绩)of a firm, the analyst invariably uses rate of return (报酬率、盈利率、收益率)analysis. This analysis, which deals with the firm's profitability(盈利能力), relates either the operating income or the net income to some base,such as the average total assets, average stockholders’ equity, or the year’s sales. The resultant percentage can be compared with similar rates for the firm in past years or to other firms. The most important relationships are:

The return on assets sometimes is called the productivity ratio (生产能力比率). It also aids management in gauging the effectiveness of its asset utilization.

The rate of return on sales varies widely from industry to industry. Some firms may operate in an industry characterized by low profit margins and high turnover of their principal assets (The ratio of net sales to average total assets is called asset turnover 资产周转率).On the other hand, firms that deal in relatively slow-moving products involving fairly long production periods require higher profit margins in order to earn a respectable rate of return on assets and on the owners’ investment. When this ratio is considered together with such relationships as return on assets and return on stockholders’ equity, much insight can be gained about the operating performance of a firm.

When analyzing the operating performance of a company, intelligent analysts make their own evaluations of the reported net income of a firm. Often, any unusual and/or nonrecurring items (such as gains and losses on sales of fixed assets or securities, casualty losses 事故损失,and the like) that have been included in the determination of net income are eliminated for analytical purposes. The analyst should also examine such factors as inventory pricing techniques and depreciation methods (and rates) to determine their effect on net income. The analyst wants to know whether the company’s net income falls in the low, or conservative (稳健的),end of the spectrum of possible amounts or whether it is on the high side. Once this is determined, it is possible to proceed to a more informed evaluation of a company’s operating performance, stock values, growth potential, and so on.

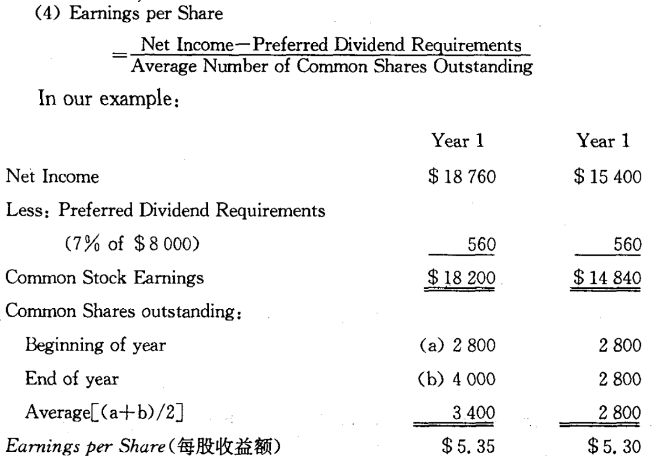

Because stock market prices are quoted on a per-share basis, it is useful to calculate a firm’s earnings on the same basis:

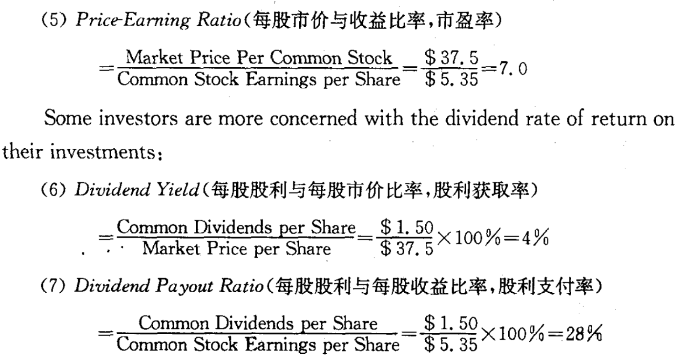

"Earnings per share for common stock" (which has been discussed in detail in the reading material of Lesson Twenty-Three) is usually given prominence in reports because both analysts and investors consider the relationship of prices and earnings to be quite important. In assessing stock values, the price-earning ratio is a useful tool :

| 以上信息有错误 |