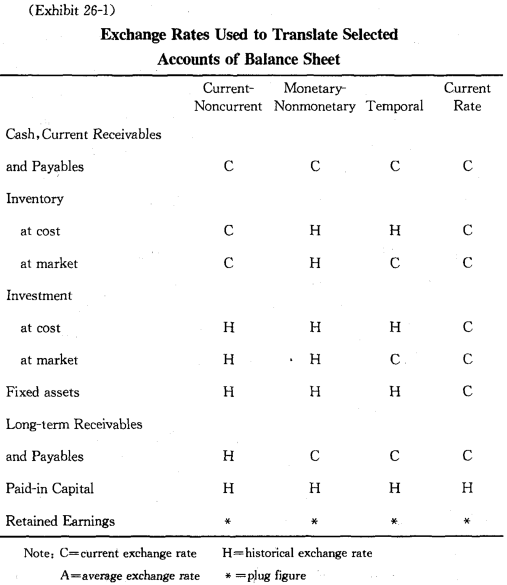

Many companies have business activities in more than one country and are referred to as multinational companies. Translation of foreign currency financial statements becomes necessary when the management of a multinational enterprise is to see the operation results of a foreign subsidiary company. Thus, the process of translation involves expressing or restating an account from one currency to another currency at the appropriate exchange rates. The four major methods used in translating foreign currency financial statements are:the current-noncurrent method, the monetary-nonmonetary method, the temporal method, and the current rate method. Exhibit 26-1 shows the various exchange rates used to translate selected accounts of a balance sheet.

Current - Noncurrent Method

Under the current-noncurrent method, current assets and liabilities are translated at current exchange rates and noncurrent assets and liabilities and stockholders’ equity are translated at historical exchange rates. The income statement is translated at the average exchange rate of the period except for those revenues and expenses items associated with noncurrent assets or liabilities. The later items, such as depreciation expense, are translated at the same rates as the corresponding balance sheet items. The method is based on the assumption that accounts should be grouped according to maturity. It is the earliest practice in the translation of foreign currency statements and is rarely adopted now.

Monetary - Nonmonetary Method

The monetary-nonmonetary method differentiates between monetary assets and liabilities—that is, those items that represent a claim to receive, or an obligation to pay a fixed amount of foreign currency units and nonmonetary, or physical assets and liabilities. Monetary items are translated at current exchange rate, and nonmonetary assets and liabilities and stockholders’ equity are translated at historical exchange rates. Income statement items except for revenue and expense items related to nonmonetary assets and liabilities are translated under the method similar to the current-noncurrent method. The philosophy behind this method is that monetary assets and liabilities have similar attributes in that their value represents fixed amount of money whose reporting currency equivalent changes each time the exchange rate changes. Examples of monetary assets and liabilities are cash, receivables, payables arid long- term debts.

Temporal Method

The temporal method requires that monetary items, such as cash, receivables, and payables, be translated at the current exchange rate. Nonmonetary assets and liabilities valued at historical cost are translated at the historical exchange rates. If they are valued at current cost, nonmonetary items would be translated at the current exchange rate. For example, inventory carried at the market would be translated at the current rate rather than at the historical rate. Income statement items are normally translated at an average rate for the reporting period. However, cost of goods sold and depreciation and amortization charges related to balance sheet items carried at historical prices are translated at historical rates. Any translation gains or losses are taken directly to the income statement. We may consider that the temporal method is an improvement based on the measurement concept to the monetary-nonmonetary method.

Current Rate Method

According to the current rate method, all balance sheet and income items are translated at the current exchange rate. Only stockholders’ paid-in capital would be translated at the historical exchange rate. Dividends are translated at the exchange rate in effect on the date of payment. Translation gains and losses are taken to a special accumulated translation adjustment account in stockholders’ equity. Thus the total amount of equity will be brought to the current rate base. This method results in translated statements that retain the same ratios and relationships that exist in the foreign currency.

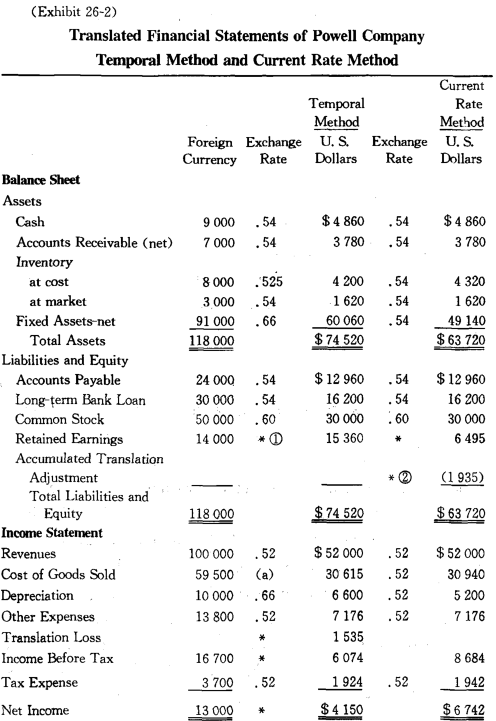

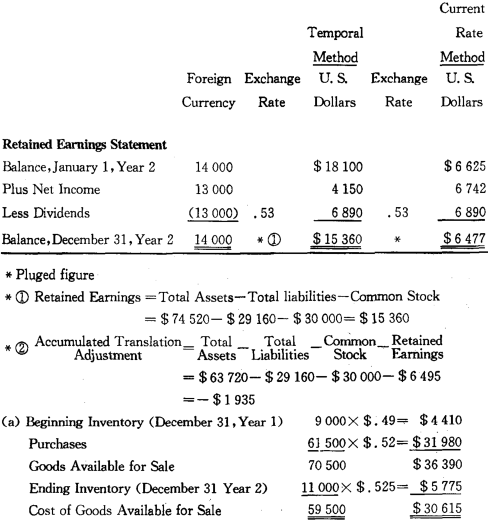

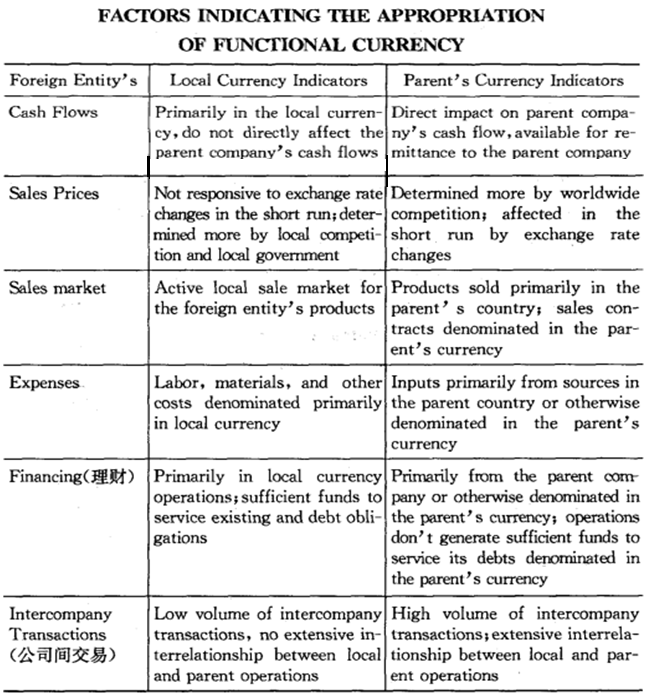

The temporal method and the current rate method are the two prevailing methods used around the world. They are considered to be the two options suitable to different natures of the foreign operations. Exhibit 26-2 shows the translation process and the translated income statement, statement of retained earnings and balance sheet under the temporal method and the current method. When the functional currency is the currency of the foreign unit which is a rather independent operating entity, the current rate method is followed. When the functional currency is the reporting currency of the parent (here assumed to be the U. S. dollar) and the foreign unit is only an extension of the parent’s operation, the temporal method is preferred. Thus, the key is to know in which currency the books and records are kept and how the functional currency of the foreign entity is defined.

New words, Phrases and Special Terms

Notes to the Text

The philosophy behind this method is that monetary assets and liabilities have similar attributes in that their value represents fixed amount of money whose reporting currency equivalent changes each time.

(1)从句that monetary assets and liabilities have similar attributes 在句中作表语。

(2)介词复杂结构in that their value represents fixed amount of money whose…修饰宾语similar attributes.

(3)定语从句whose reporting currency equivalent changes each time 修饰fixed amount of money.

READING MATERIAL

| 以上信息有错误 |